Excellent adviceYour questions are common and valid. And I agree that the information in the screen shot isn't presented terribly clearly. So I'll give you my interpretation, but you need to consult with your HR department for a final ruling. I promise, they get those questions all the time and are used to answering them.

A few things to start:

First, your company offers a choice between a traditional 401k and a Roth 401k. That's a good thing. It's also separate and apart from the Roth IRA you have at Morgan Stanley -- two totally different things.

Second, my reading of the second sentence under Employer Match is that your company unfortunately doesn't match your contributions up to 5% of your salary. They match 50% of your contributions to the extent of 5% of your salary. Effectively, a cap on the match of 2.5% of your salary. That's still good. You get 7.5% in your account, but only have to contribute 5%. That's a 50% return on that portion of your contributions. While it's not as good as a 100% match, it's still way better than you can get anywhere else out on your own.

Third, the information doesn't explicitly say that the match applies to the Roth 401k option. I'd have to think it probably does, but you need to verify that with your HR department.

The answer to your question about what happens if you contribute $10,000 depends on your salary.

Let's say your salary is $75K a year, and that you contribute $10K into the 401K the first year you're eligible.

5% of your $75K salary is $3,750. Your company matches that at 50% -- or $1,875. Plus, you're contributing an additional $6,250 that isn't getting matched (the difference between $10,000 total you're putting and the $3,750 that is getting matched).

So you end up with a grand total contributed into your account of:

$3,750 the part of your $10K contribution that's eligible for your company match, plus

$1,875 the dollar amount that your company puts in as your match, plus

$6,250 that you contribute on top of what is being matched

$11,875 Grand Total Contributions

Obviously, you'd need to adjust those numbers to reflect your actual salary.

A few additional thoughts:

1. I hear a lot of young people (and some older ones) say that they've "maxed out" their 401k contributions when they do enough to get the full company match. Unless their salary is well over $250K, that's garbage. You're not "maxed out" until you're contributing the maximum the IRS allows -- in 2019 that's $19K, and $25K if you're over 50.

Admittedly, that's not easy to do. Here's how Mrs. Basket Case and I did it: We started out contributing all we could. On top of that, we effectively didn't get a raise for several years. What I mean is that every time we got a raise, we increased our 401k contribution by the amount of the raise. We did that for about 6-7 years, and finally got there. It was a pain for a while, but soon enough it was built into our lifestyle, and largely painless. The reward at the end of that time -- a really nice start on a retirement nest egg -- was incredibly gratifying.

2. Use debt wisely. Borrow as little as you possibly can to buy depreciating assets (like a car). Buy used. Don't ever borrow to fund experiences -- vacations, concert tickets, dinners out, etc. If you put that stuff on a credit card to get miles or bonus rewards, be sure to pay it off every month -- if you can't do that, you can't afford whatever it is. The first time you have a credit card bill made up of experiences, and you can't pay it off in full, that should be a big, loud, whanging wake-up call.

If you borrow to buy a house (and almost nobody can pay cash for their first one), have the payment on a 15-year schedule, not 30. Later, if you upgrade your house, keep the payment on the original schedule. Example: say you buy your first house and have the 15-year schedule. Three years later, you upgrade to a nicer house. Your payment schedule on the new house is 12 years. Three years later, you upgrade again. That mortgage is on a 9-year schedule. The idea is to have whatever house you're in at the time debt-free 15 years after your first purchase.

I don't agree with Dave Ramsey on everything, but he's got the debt thing right. Live like nobody else for a while, so you can live like nobody else forever afterward.

3. Ignore jackasses braying at social gatherings about their new cars, their vacations, their house, whatever. Almost invariably, they're selling their souls to impress you. Be far more concerned with impressing yourself than bragging to others. You'll be amazed how often those same public braggarts come to you in private, after the party's over, asking for advice on their impossible financial situation....in other words, you're actually impressing them far more than they want the world to know.

4. Don't confuse gambling with investing. Never have more than 10% of your portfolio in any one investment. Diversify, diversify, diversify.

5A. The most important thing: Start young, as you already have. Keep it up. For you, time is your most valuable asset. But it is also your most perishable. People that spend everything they can while young wake up at about age 40-45 and realize that they're in deep trouble, with nowhere near enough time to work themselves out of it.

5B. I know it seems counter-intuitive, but while you're young, recessions are actually your friend. You keep on keeping on with your investments, buying stocks while they're down. Later, when the recession lifts and the stock markets come back (and they always do), this is where you really make hay on the stuff you bought cheap while everybody else was scared and not investing at all. During a recession, turn off the TV news, keep your head about you, and keep on investing. This doesn't hold if you're 5 years or less out from retirement, but at your age it definitely does.

Yes, it's hard. And it takes between 7 and 10 years to really start seeing the rewards. I liken it to starting a bike ride in 21st gear. It's hard, and you're putting out a lot of effort, and not getting much of anywhere early on, and it sure would be easier to just get off the [stupid] thing. But gradually it gets easier and easier until finally you're cruising along at a pretty sporty clip.

It's not easy, but nothing worthwhile ever is. And the financial and emotional rewards in the end are just incredible. OK, off the soapbox.

Personal Finance Advice for Roth and 401k

- Thread starter Jessica4Bama

- Start date

And well presented. It left the tax attorney with nothing to add...Excellent advice

4Q with some awesome advice, again!

Also, extending 4Qs first point, the real maximum is more like $54k... which, if you had a side business you could create a Solo 401k and contribute there as well. Also, 401k plans may allow after tax contributions, and Roth IRAs allow so-called back door and mega back door contributions. You’ll want to know these exist when you’re running the hospital or taking in lots of side hustle $$

The above are obviously not following my previously stated simple rules and generally only make sense at high income and/or executive-level pay or small business owner with good profitability so don’t worry about them anytime soon but could be of help to somebody on here.

Sent from my iPad using Tapatalk

Also, extending 4Qs first point, the real maximum is more like $54k... which, if you had a side business you could create a Solo 401k and contribute there as well. Also, 401k plans may allow after tax contributions, and Roth IRAs allow so-called back door and mega back door contributions. You’ll want to know these exist when you’re running the hospital or taking in lots of side hustle $$

The above are obviously not following my previously stated simple rules and generally only make sense at high income and/or executive-level pay or small business owner with good profitability so don’t worry about them anytime soon but could be of help to somebody on here.

Sent from my iPad using Tapatalk

Last edited:

Goodness all this is confusing. Haha. The reason I worry about it is I'm single and I don't see myself ever marrying, so my income is what has to sustain me when I am old. One of my fears is living paycheck to paycheck and not being able to afford a house or retire or afford things I need and the list goes on. I'm not one who looks too far into the future. I am more of in the moment type of person, but the thought of not having enough money to live on in retirement strikes fear in me. I have always been one who has saved money. I currently have no debt, but will be looking for a house soon, which I am hoping to be able to put between 20-30% down. I do pay off my cards monthly, so no interest fees for me. But all this investing stuff really confuses me.

Last edited:

Also, on a side note that I thought was interesting. I recently watched a segment on the today show who had some financial guru. They said if you put away $200 a month starting at age 30 in a Roth IRA, by the time you are 70, it would have gained up to 1.2 million. I guess that is based on the current returns each year, which could go up or could go down. But I thought that was an interesting tidbit. A lot of 30 plus year olds may not be able to contribute that much, but it sure makes me want to invest what I can now while I am still in my early 30s.

If you have no debt and pay your cards off monthly, you already have the right hard-wired mindset. Don't let all the details paralyze you.Goodness all this is confusing. Haha. The reason I worry about it is I'm single and I don't see myself ever marrying, so my income is what has to sustain me when I am old. One of my fears is living paycheck to paycheck and not being able to afford a house or retire or afford things I need and the list goes on. I'm not one who looks too far into the future. I am more of in the moment type of person, but the thought of not having enough money to live on in retirement strikes fear in me. I have always been one who has saved money. I currently have no debt, but will be looking for a house soon, which I am hoping to be able to put between 20-30% down. I do pay off my cards monthly, so no interest fees for me. But all this investing stuff really confuses me.

Invest everything you can for 30 years, including increasing the amount invested as your income rises. Don't worry about recessions or downturns in the markets until you're about 5-7 years from retirement. As I mention above, these are the times young people can really make huge progress toward their long term goals. If you do all that, the power of compounded returns will take care of you.

And as someone posted earlier, take some time to smell the roses along the way. Just don't overdo it, confusing wants with needs. For example, you may actually need some time off...a few days at the beach. Do that a couple of times a year. While you may want it, you don't need 10 days at the Grand Floridian in Orlando, or a week on South Beach at the Delano.

Last edited:

You are on the right track, no debt with savings and retirement in place, you are way ahead of most Americans. Life, like dieting, is all about moderation, make a budget, stick with it and adjust as needed. You do not appear to be an extravagant person, but every once in a while you need some chocolate.Goodness all this is confusing. Haha. The reason I worry about it is I'm single and I don't see myself ever marrying, so my income is what has to sustain me when I am old. One of my fears is living paycheck to paycheck and not being able to afford a house or retire or afford things I need and the list goes on. I'm not one who looks too far into the future. I am more of in the moment type of person, but the thought of not having enough money to live on in retirement strikes fear in me. I have always been one who has saved money. I currently have no debt, but will be looking for a house soon, which I am hoping to be able to put between 20-30% down. I do pay off my cards monthly, so no interest fees for me. But all this investing stuff really confuses me.

Also, on a side note that I thought was interesting. I recently watched a segment on the today show who had some financial guru. They said if you put away $200 a month starting at age 30 in a Roth IRA, by the time you are 70, it would have gained up to 1.2 million. I guess that is based on the current returns each year, which could go up or could go down. But I thought that was an interesting tidbit. A lot of 30 plus year olds may not be able to contribute that much, but it sure makes me want to invest what I can now while I am still in my early 30s.

Yep! That assumes a 10% average return over 40 years. This is about the market average over the last 100+ years. That's history and nothing is guaranteed going forward (which is why I use 4% in my planning - especially since I'm older than you

Since you're invested for the long term you really don't care what happens year-to-year so long as the market goes up over the next 40 years. If you could put $500/mo to max out your Roth and it "only" returned a 7% per year average over 40 years you would still get to your target. Then if the market ended up returning 10%, you'd have >$3million. Obviously, Roth wouldn't be your only investment as your salary increases. You'll have 401k, and at some point probably a 457b or 403b (similar to 401k with some different features / constraints), deferred comp, profit sharing, after tax (i.e. just going to Fidelity.com and buying funds), etc. Your commitment to starting now and continuing for the next 30+ years is what will get you to your goal. We've given you LOTS to consider. I know it's overwhelming. It's all based on experience (some good, some bad!) and market truths and solid research. Some of it is stream of consciousness from me (and thinking of others who might read this and benefit, as well). I'll try to boil down my thoughts here...

To keep it simple:

0) Read this: https://www.bogleheads.org/wiki/Bogleheads®_investing_start-up_kit . This is succinct and actionable.

The key to understanding is educating yourself (Boglehead's first step). Most likely you, like me, will be confused the first time you read this stuff. So, you read more and more until it starts to make sense. But you don't wait to invest.

In your 401k and/or Roth go ahead and put your contribution in a target fund (i.e. one that is called something like Fidelity 2050 Target Fund or whatever they call it). You can change it later to be aligned with what you learn. In a retirement fund, you don't have to worry about changes requiring you to pay taxes. [In an after-tax fund (i.e. at a broker) capital gains taxes must paid.]

1) Decide how much you are willing to invest each month. At a minimum, contribute the 5% of your salary that will be matched at 50%.

2) Decide your "risk tolerance." Some call this a 'sleep number' as in "what are you comfortable investing in equities (stocks) so that you can sleep at night without worrying what the market is doing." There are a bunch of theories on what the percentage should be, but the longer you have to invest (i.e. 30+ years is along time), the more your portfolio can tolerate ups and downs of the market - but this is a personal decision! Some suggestions are if you have a high risk tolerance, then have an aggressive equity allocation: 120 minus your age (or 110 if you're moderately aggressive or 100 if you're conservative). This is the percentage of your investment that should go into stocks funds the rest in bonds. So for moderately aggressive if you're 30 then 120-30 = 90, 110-30=80 etc).

3) Decide your asset allocation (considering your risk tolerance). If you decided to be aggressive, 90% of your monthly contributions would go into equities and 10% into a bond fund. You should also decide if you want to do international stocks. I suggest you do to get complete diversity, but some folks (Jack Bogle included) said you don't need them.

4) Decide which funds to buy (considering your asset allocation). If you choose to do the 3-fund portfolio, your breakdown might look like below.

Here's an example of a moderately aggressive 3-fund portfolio allocation:

80% in equities: of this 70% would be in a total stock market index and 30% in a total international stock market index.

20% in bonds - in a total bond market index.

I don't know what funds you have available in your 401k/roth/etc. but if it is Fidelity Funds, then each month (or paycheck) your contribution might be allocated into these 3 funds (again depending on which specific funds are available to you and your risk tolerance).

This is based on an 80/20 split:

56% in Fidelity Total Stock Market Index (FSTMX)

24% in Fidelity Total International Stock Market index (FTIGX)

20% in Fidelity Total Bond Fund(FTBFX)

Alternatively, you could choose to keep it REALLY simple by choosing a target date fund for the year (approximately) you plan to retire. The fund manages the splits/allocations.

4) Don't go with "whatever fund has been up the most in YTD/1/3/5/10 years". Choosing the total market path (either 3-fund or 1 target fund ) keeps it very simple. You set it and forget it and just check it every now and then. Don't buy expensive funds. Diversify by buying the total stock and total bond market. These are usually the cheapest funds available to you. Check out the The Callan Periodic Table of Investment Returns to understand how last year's winner is this year's loser (and vice versa) over last 20 years (and month-to-month)

5) Stay the course! Don't worry about the market's ups and downs. 4Q has done a great job of detailing how his family approached this. Increase your investment amount as you can when you get raises, promotions, bonuses. Keep reading & learning.

6) Retire comfortably

4Q's advice regarding debt is outstanding. Wish I had considered this when I got my first real job and thought I was rich!

Also, only "worry" about the things you can control: How much you save and how much you spend.

Last edited:

Something else that helps is actually (and systematically) going through an analysis and documenting what you're doing and why.

We do this in our Investment Policy Statement (IPS). You can find generic versions & templates on the internet at Bogleheads, Morningstar, Vanguard, etc. Our own (see attached template which contains our basic structure and some examples) takes what we think are the best parts from all of these and is mostly based on the Morningstar one and some Bogleheads examples.

We do this in our Investment Policy Statement (IPS). You can find generic versions & templates on the internet at Bogleheads, Morningstar, Vanguard, etc. Our own (see attached template which contains our basic structure and some examples) takes what we think are the best parts from all of these and is mostly based on the Morningstar one and some Bogleheads examples.

Attachments

-

252.9 KB Views: 1

It's also a good idea to determine what type lifestyle you want to keep when you retire. Granted, as young as you are this could change several times over the course of your life.

This will dictate how aggressive and for how long you'll need to be over the lifetime of your investing. My aunt and uncle (who are very simple people) decided about halfway to retirement they didn't want as "lavish" of a lifestyle as they did when they first started planning. So they weren't as aggressive the last half of their careers. They changed gears a bit and decided to enjoy life a little more as they went rather than "maxing out" contributions all the way to retirement. They currently are entering retirement age, have paid off their house, they have zero credit card debt and zero car notes. I don't know how much money they forfeited by backing off their contributions halfway through their work careers. But as long as they are happy and content, they made the right choice.

This will dictate how aggressive and for how long you'll need to be over the lifetime of your investing. My aunt and uncle (who are very simple people) decided about halfway to retirement they didn't want as "lavish" of a lifestyle as they did when they first started planning. So they weren't as aggressive the last half of their careers. They changed gears a bit and decided to enjoy life a little more as they went rather than "maxing out" contributions all the way to retirement. They currently are entering retirement age, have paid off their house, they have zero credit card debt and zero car notes. I don't know how much money they forfeited by backing off their contributions halfway through their work careers. But as long as they are happy and content, they made the right choice.

You've already done the single most important thing -- you got started young.5) Stay the course! Don't worry about the market's ups and downs. 4Q has done a great job of detailing how his family approached this. Increase your investment amount as you can when you get raises, promotions, bonuses. Keep reading & learning.

6) Retire comfortably

Aside from that, unless it's literally a choice between investing vs. eating / keeping a roof over your head, the most important thing is not to stop. Not ever. No matter what noise the squawk box is spewing.

Market swings are by definition temporary. They go up. They go down. Acknowledging scary periods of time, over the long term, there is a decided bias up. That bias up is what distinguishes investing from gambling.

Make your plan. Adjust it periodically for life events -- marriage, children, taking in a relative, etc. But, no matter what's going on in the markets or how bad they look, don't let market fluctuations scare you into deviating from your plan. If you have the spare cash, invest more when there's blood in the streets....even if some of that blood is yours. You can never truly call yourself an investor until you've persevered through a bear market, and come out on the other end stronger emotionally, and even better off financially, than you were when it started.

Believe me, I know how easy that is to say, and how hard it can be to do. It was first quarter of 2009, and I was doubting. So many talking heads were saying, "It's different this time." But so many more knowledgeable people were pointing out that the best deals are made in the worst of times. I gulped, closed my eyes real hard, and Mrs. Basket Case and I stayed the course. Want to know the irony of all that? Investing through The Great Recession and the ensuing recovery made it possible for me to retire.

Last edited:

Out of all the already great advice given, this is also very important. Never quit/give up. There will/may be times in your life when unexpected life events (job loss, cuts in pay etc.) forces you to go through a season of only being able to contribute $200/month rather than $500/month. Still put in. Something is better than nothing. Don't get discouraged. Keep putting in SOMETHING.You've already done the single most important thing -- you got started young.

Aside from that, unless it's literally a choice between investing vs. eating / keeping a roof over your head, the most important thing is not to stop. Not ever. No matter what noise the squawk box is spewing.

Market swings are by definition temporary. They go up. They go down. Acknowledging scary periods of time, over the long term, there is a decided bias up. That bias up is what distinguishes investing from gambling.

Make your plan. Adjust it periodically for life events -- marriage, children, taking in a relative, etc. But, no matter what's going on in the markets or how bad they look, don't let market fluctuations scare you into deviating from your plan. If you have the spare cash, invest more when there's blood in the streets....even if some of that blood is yours. You can never truly call yourself an investor until you've persevered through a bear market, and come out on the other end stronger emotionally, and even better off financially, than you were when it started.

Believe me, I know how easy that is to say, and how hard it can be to do. It was first quarter of 2009, and I was doubting. So many talking heads were saying, "It's different this time." But so many more knowledgeable people were pointing out that the best deals are made in the worst of times. I gulped, closed my eyes real hard, and Mrs. Basket Case and I stayed the course. Want to know the irony of all that? Investing through The Great Recession and the ensuing recovery made it possible for me to retire.

Jessica, I commend you on asking the right questions and trying to do the right thing! Keep up the good work!!!

Too bad more people, a lot more people, aren't as disciplined as you.

Too bad more people, a lot more people, aren't as disciplined as you.

Since we’ve been discussing this, I wanted to link here to an article on whitecoatinvestor.com [WCI] today discussing this very topic:

https://www.whitecoatinvestor.com/r...the-critical-concept-of-filling-the-brackets/

WCI is mostly written for high net income folks (it’s written by and for doctors) but he does a great job in explaining details and giving good examples regardless of income level. Might be useful for some on here

Sent from my iPad using Tapatalk

https://www.whitecoatinvestor.com/r...the-critical-concept-of-filling-the-brackets/

WCI is mostly written for high net income folks (it’s written by and for doctors) but he does a great job in explaining details and giving good examples regardless of income level. Might be useful for some on here

Sent from my iPad using Tapatalk

To really simplify this, probably easier to just choose a target retirement date fund and let it reset the allocations for you automatically. Then you don't have to worry about allocations if that's all you have invested. Once you have additional investments (after tax, roth, IRA, etc) then you'll need to figure out your overall strategy. Get the match at least if offered.

I'll also throw these short reads back out there:

Just as an FYI example to show how powerful compounding and matching is (and not knowing any of your salary, etc)...

If your salary is $50K/yr and you put 15% into 401k and your employer matches 50% of the first 6%, with a 2% average annual salary increase, a 7% annual return on average, in 30 years you'll have about $1.6 million.

Contribute early, often, and continuously.

I'll also throw these short reads back out there:

- Bernstein's "If You Can": https://www.etf.com/docs/IfYouCan.pdf

- My "Invest for Retirement" suggestions: https://news.tidefans.com/invest-for-retirement/

- A decent 401k calculator: https://www.bankrate.com/calculators/retirement/401-k-retirement-calculator.aspx

Just as an FYI example to show how powerful compounding and matching is (and not knowing any of your salary, etc)...

If your salary is $50K/yr and you put 15% into 401k and your employer matches 50% of the first 6%, with a 2% average annual salary increase, a 7% annual return on average, in 30 years you'll have about $1.6 million.

Contribute early, often, and continuously.

Last edited:

I decided to start out putting 8% into my 401K. I went with the Roth option because once I retire I will definitely be in a higher tax bracket than what I am now being nurses in Alabama doesn't make much starting out compared to other states. I was worried about putting 15% into it because I am looking to buy a house sooner rather than later. Maybe I should go ahead and put the 15% into it, but since nurses in Alabama don't make much money as a new grad, I was thinking 8% may be a happy medium. I need to be able to afford my house. LOL.

Also, I had no idea how to allocate my funds, so Fidelity had a blended Vanguard target 2050 that I started with. Hope that is a good one to put my money into. It appeared to have a good track record from what I could see.

Also, I had no idea how to allocate my funds, so Fidelity had a blended Vanguard target 2050 that I started with. Hope that is a good one to put my money into. It appeared to have a good track record from what I could see.

Especially while you're young and new to the plan, the targeted fund is a great choice. It'll be almost 100% stocks, which is what you want at your stage in life and career.I decided to start out putting 8% into my 401K. I went with the Roth option because once I retire I will definitely be in a higher tax bracket than what I am now being nurses in Alabama doesn't make much starting out compared to other states. I was worried about putting 15% into it because I am looking to buy a house sooner rather than later. Maybe I should go ahead and put the 15% into it, but since nurses in Alabama don't make much money as a new grad, I was thinking 8% may be a happy medium. I need to be able to afford my house. LOL.

Also, I had no idea how to allocate my funds, so Fidelity had a blended Vanguard target 2050 that I started with. Hope that is a good one to put my money into. It appeared to have a good track record from what I could see.

That desired mix evolves as retirement approaches. So if the fund is managed correctly, its mix will likewise evolve accordingly, gradually trading out of stocks and into bonds and other less volatile instruments. That's a gradual process, taking place over a number of years, with the first baby steps starting for a 2050 fund around 2035 or 2040.

Congratulations on asking the right questions, and taking action, all while you still have your most important asset...time. So many people put their fingers in their ears and hum. Then one day, they hit 40, and say, "Oh, [lots of non-TF words]....I've got to get started!!"

Trouble is, they already frittered away the most powerful thing they had: their investing youth.

The consequences are both unforgiving and incredibly sad. These are the guys who, when they hit 62-65, are going to their colleagues' retirement parties, saying they'll have to work until they drop. It's so sad because it's so avoidable.

Last edited:

Which of these would you recommend me adding to my allocation of funds? I have the target 2050 option, but Fidelity told my coworker that wasn't a great one. Any help you be appreciated.

Hey @Jessica4Bama - I was going back through some of these personal finance threads and realized you never got an answer to your last question. The Target 2050 fund assumes you're retiring in 2050 and will, over time, adjust automatically (rebalance) from equities to bonds/fixed income.Which of these would you recommend me adding to my allocation of funds? I have the target 2050 option, but Fidelity told my coworker that wasn't a great one. Any help you be appreciated.

Not sure why Fidelity would say of VFIFX that "it's not a great one" other than because they don't get paid very much because the expense ratio is only 0.08% - that's a great rate IMHO for a fund like this. Anytime you can have expense ratio of <0.10% you're doing it right most of the time. Jack Bogle always said "You get what you don't pay for" (meaning expenses matter!)

Also, don't try comparing returns from one fund to another because they're trying to achieve different things and, thus, will have different risk / return profiles; it's also like driving forward while looking backward.

So, not sure what you've decided to do in the last year since you started, but hopefully you're in the 2050 or something similar.

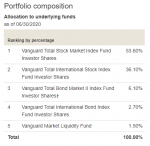

The current composition of the 2050 fund (VFIFX)is the following:

Latest threads

-

Maybe aTm's Pockets Aren't So Bottomless After All -- Layoffs In The Athletic Department

- Started by 4Q Basket Case

- Replies: 1

-

Time to un-vacate 2005-2007 on field victories and un-forfeit the 1993 season?

- Started by CmdrThor

- Replies: 9

-

-

-

SIAP there was an article that Joe K interviewed for assistant coach

- Started by mlingerfelt31

- Replies: 11

-

Final Home Midweek for Alabama Brings Samford to The Joe

Final Home Midweek for Alabama Brings Samford to The Joe- Started by Diamond Tide

- Replies: 0