We are talking past one another, so I'm out.I'm not disparaging anyone, other than suggesting the 'college for everyone' mantra is a false one and people should be able to do the basic math and understand whether or not it's a wise investment.

If they're incapable of that, that's on them. That's not making a disparaging remark, that's simply acknowledging fact.

People make poor decisions all the time, I'm not sure why I (and my kids and their kids) should be on the hook for them. We're not talking about people starving to death here, we're literally talking about them not having the lifestyle they'd like due to the decisions they made.

So yes, I disagree with your conclusion, and no, that doesn't make me wrong or somehow 'missing the truth'.

Cancelling student loans?

- Thread starter AlistarWills

- Start date

That is I think the fundamental disconnect.People make poor choices daily, it's what they do. But literally anyone who chooses to take on six figures of debt without a pretty good idea as to how they will pay that off likely shouldn't be in college.

Comparing that - something that is largely within their control - with the randomness of something like a pandemic is again essentially suggesting that no one should be held accountable for anything that happens t them, because who could have seen that coming?

When these kids took these loans, they did not have the financial nor personal planning wherewithal to recognize that:

1. Taking out an exorbitant amount of debt would financially cripple them.

2. The state of the economy, economic crashes, and the like made the available white collar job pool shrink due to older people staying in the work force longer due to their own poor planning.

3. College != success

I think it would be fair to say that the US education system is essentially on a rail. You get into the system, and continuously build upon prior knowledge and dogma until at some point around 18 you get to take some exams that determine how well you are prepared for college. Nearly all students take these exams, because that is "just the thing you do after high school."

At no point along this rail have these kids been exposed to the idea that they can question the path they are on. At least not by the system that is merrily moving them along their educational path. They are continually exposed to media showing them how great college life is, how all of these kids are living it up and having the best time in their life. College is their reward for making it through the US educational system. What is the harm in getting some student loans to make college life a little more enjoyable? Everyone says the only good kinds of debt are house and school debt. This is definitely school debt, and the people pushing the degrees at their college of choice assure the kids that once they graduate a whole wide world will open for them and companies will be falling all over themselves to offer them good paying jobs. Not all of those loans are even going to quality of life, they are going to actual tuition, which has also increased as colleges realize that they are no longer selling diplomas but a quality of life.

You may look at the above and say that is obviously false. There is no way that that rosy picture is what kids coming through the system actually believe. And for your experience, or your own children, or your own experiences with kids who went to college that may not actually have been the perception when they were in school or preparing for school. However there are many kids who approach college with just that mindset. And according to this article there are many parents who are following their children down the college debt trap.

So if the kids were never taught to be on the lookout for what amounts to a bad deal, and the people who were supposed to be teaching them are themselves unable to recognize a bad deal. In effect continuing the escalation of commitment, where is the offramp? Does it really make sense to financially hobble several generations down a system that is broken for all but the most fiscally savvy?

I don't have an easy solution. I will say that I am not in the group that believes 50k in debt relief is the solution. I am not sure I believe 10k is the solution. If I were to pick any solution that I thought had a real chance of solving the problem, it would be Buttigeig's service corp suggestion during his campaign.

One final aside. I do think that there are many who think that these people who took out all these loans made their bed and should lie in it. I am not sure that many truly understand the ramifications on older generations, or if they do, they are willfully ignoring some of the significant issues that will arise. With many of these people unable to get started, they are unable to build wealth in one of the traditional American wealth building models. That of home ownership. People who are sitting on expensive houses have to realize that they won't be there forever. If there is no subsequent generations to pick up the torch and buy their house when they are ready to downsize their home values will go down. Which reduces what amounts to a good portion of the nest egg that many older Americans have managed to save over their life.

American Homeowners Need a New Retirement Plan said:Banking on home for retirement

Homes also figure prominently in Americans’ retirement planning. A quarter of American homeowners (25%) are planning to use their home as an asset to fund their retirement. Forty-two percent of those say their home is one of the top four most important ingredients in their retirement plan, and one in 10 of those say it’s the biggest part of their retirement plan.

Among those who are planning to sell their home or tap their home's equity to fund their retirement, home equity represents a big chunk of their retirement nest egg. Of these, 17% say their home represents half or more of their retirement nest egg; 38% say their home represents 26-50% of their retirement nest egg; another 35% say it represents 5-25%.

Among those planning to sell their home to fund their retirement, 38% say they’ll move to a less expensive area with a lower cost of living. 21% say they’ll purchase a smaller home nearby, and 12% will move to a retirement home or community. 7% plan to rent, and 4% say they’ll move to a less expensive country. Only 1% plan to live with a child, and 14% don’t know yet what they will do.

Planning on home price appreciation

Homeowners are generally optimistic about home prices. Almost three-fourths of homeowners (70%) think their house will be worth more by the time they retire: 35% think it will be worth 10% more, another 25% think it will be worth 25% more, and an optimistic 8% think it will be worth 50% more. Just 12% of people think their house will be worth the same when they retire as it’s worth today, and only 4% think the value might decrease.

Almost two-thirds (64%) of people planning on a value increase in their home before retirement say that expected increase is important to their plan to retire. One in five (19%) say it’s very important, and 2% say that without that expected increase in home value they’ll be unable to retire. While 61% of Americans say a 25% drop in home values wouldn’t impact their retirement plans at all, it would delay retirement for the other 39%: 19% say that if their home dropped 25% in value, they’d have to delay their retirement by a year or two, 13% by about 5 years, 3% by about 10 years, and 3% say they’d be unable to retire.

Nothing is free. Somebody has to pay for it.We have one group that sees people in need and another that sees deadbeats. You can't reconcile that kind of gap.

I have watched bout dozen documentaries on the working model of free college education. Sadly, if Americans can't profit from it, Americans think it is socialist or in some other way seriously flawed.

Why is America no longer the shining beacon? Because Americans have been abandoned by the rich, and the foolish who have been conned into helping make the rich richer.

When I was in Argentina a couple years ago, when everyone was extolling their "always free" university education, I made a point of reminding them that it wasn't "free". Somebody had to pay for it, and their economic problems had made that a lot more problematic.

That being said, I do believe that we could at least guarantee pre-qualified (grades/ACT/SAT) students a couple of years at community college. Lessen the blow of a 4-year degree immensely. Maybe put some service stipulations in there as well.

I have read thru this thread a bit. Yeah, yeah, we had to eat dirt when we were in college, and we liked it.

")

All kidding aside, education costs have skyrocketed over the past several decades. It's a lot more expensive than when I was in college.

I am fiscally conservative enough to believe that the government cannot solve all of our social and financial ills by throwing money at the issue.

My preference would be to have a discussion about how we as a country begin to address the issues created by having so many young people without job opportunities due to extremely poor reading and math skills. Literacy is a central issue in societies such as ours with such a large population of poor.

I would advocate for spending our money and teaching resources in getting our young people directed toward technical and vocational training to enable them to actively participate in the economy and raise themselves from poverty. I would support as a minimum every student receiving at least two years of post high school education aimed at filling critical skills required in the economy.

I am no educator but do believe that there are templates available in other countries such as Germany that have been very successful so that it isn't necessary for us to reinvent the wheel.

My preference would be to have a discussion about how we as a country begin to address the issues created by having so many young people without job opportunities due to extremely poor reading and math skills. Literacy is a central issue in societies such as ours with such a large population of poor.

I would advocate for spending our money and teaching resources in getting our young people directed toward technical and vocational training to enable them to actively participate in the economy and raise themselves from poverty. I would support as a minimum every student receiving at least two years of post high school education aimed at filling critical skills required in the economy.

I am no educator but do believe that there are templates available in other countries such as Germany that have been very successful so that it isn't necessary for us to reinvent the wheel.

The rate of tuition cost increases at universities have doubled and tripled the rate of inflation over several decades without them delivering a better product over that time period.Nothing is free. Somebody has to pay for it.

When I was in Argentina a couple years ago, when everyone was extolling their "always free" university education, I made a point of reminding them that it wasn't "free". Somebody had to pay for it, and their economic problems had made that a lot more problematic.

That being said, I do believe that we could at least guarantee pre-qualified (grades/ACT/SAT) students a couple of years at community college. Lessen the blow of a 4-year degree immensely. Maybe put some service stipulations in there as well.

I have read thru this thread a bit. Yeah, yeah, we had to eat dirt when we were in college, and we liked it.

All kidding aside, education costs have skyrocketed over the past several decades. It's a lot more expensive than when I was in college.

Tennessee does this already - it works well, though there are still kids who turn their nose up at FREE community college for two years and instead go to the major public schools for all four years, amassing debt the entire time.That being said, I do believe that we could at least guarantee pre-qualified (grades/ACT/SAT) students a couple of years at community college. Lessen the blow of a 4-year degree immensely. Maybe put some service stipulations in there as well.

I agree with much of what you say here, and fundamentally agree - I've said throughout this thread that unless / until we fix the underlying issues, we're just throwing money away.That is I think the fundamental disconnect.

Long term effects on the older generations are balanced by the long term effects on the youngest generations, or even those not born yet. We obviously don't live in a vacuum and if we don't curb the massive spending we've seen over the last few decades (in particular), at some point the average US citizen will pay for it. And it will be catastrophic - far worse than anything we've see to date.

I feel for those who thought they were on their way to 'successful' lives only to find they were mistaken, or the goalposts were moved, or whatever happened. But we don't have an endless supply of money, so I think we need to focus on fixing the underlying issues that make universities act like for for-profit businesses rather than slapping a band-aid on a gaping chest wound.

i haven't checked it out, but my guess would be that entry level wages for college graduates have not really kept up over the past few decades.The rate of tuition cost increases at universities have doubled and tripled the rate of inflation over several decades without them delivering a better product over that time period.

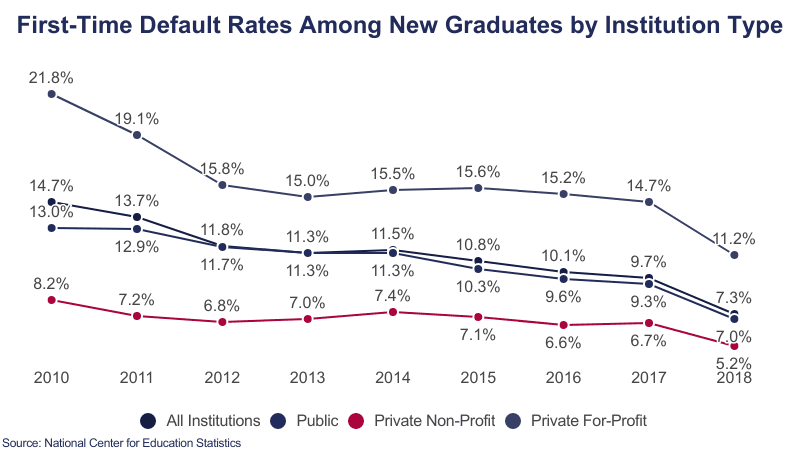

this link has a lot of stats on defaults

educationdata.org

educationdata.org

National Student Loan Default Rate [2023]: Delinquency Data

An analysis of student loan default rates along with financial consequences and solutions for students with loans in default.

Outside of a few fields, that's correct.i haven't checked it out, but my guess would be that entry level wages for college graduates have not really kept up over the past few decades.

Engineering and medical have both done pretty well. Engineering in particular still seems to have difficulty in getting enough qualified people in the field.

Women's Studies | Data USA

In 2021, the locations with the highest concentration of Women's Studies degree recipients are Madison, WI, New York, NY, and Gainesville, FL. In 2021, the locations with a relatively high number of Women's Studies degree recipients are Aurora, NY, Northampton, MA, and Grinnell, IA. The most...

datausa.io

datausa.io

2,723 degrees in women's studies were awarded in 2017. the average salary for folks with women's studies degrees is $75k. lots of other interesting stats at the site, although nothing on student loan default rates.

In 2014-2015, approximately 1.9 million bachelor’s degrees were awarded.

Of those:

- Just 1,333 degrees were in women’s studies, the most common “useless major” bogeyman that grumpy readers write me about.

- 7,782 degrees were in the broader category of “area, ethnic, cultural, gender, and group studies,” which women’s studies falls under. This represents about 0.4 percent of all bachelor’s degrees.

- 2,868 degrees were awarded in art history. In the broader category of any visual/performing arts field, there were 95,832 degrees, or about 5 percent of all degrees given.

- 248 degrees were in in “English literature (British and Commonwealth),” the closest category to “12th-century English poetry.”

- 45,847, or about 2 percent, were in the broader category of all English language and literature/letters.

- No stats on basket-weaving per se, but 187 BAs were given in “fiber, textile and weaving arts.”

Thank you for sharing that...really eye-opening. Destroys a lot of the "myths" that many of us believed...

The stats don’t sound as good as a Hannity or Carlson Fox News zinger to rile people up about those lazy Millenials.Thank you for sharing that...really eye-opening. Destroys a lot of the "myths" that many of us believed...

America was at it's greatest when it wasn't throwing money at every problem as if that solved the underlying issues. That's what's changed. Seems like most think the answer to everything is more government spending - the decline of the US in the world started with the massive deficit spending in the 80s and has gone down hill since. That is not a coincidence. The underlying issues remain untouched while our kids and grandkids standard of life will be greatly diminished due to us throwing literal trillions at everything.

Arguably, America was at its greatest when it directed the money it spent toward the people and began its decline when it spent less on people and more on corporations and "defense". It is no coincidence that the huge tax cuts for the wealthy, huge increases in defense spending, curbing of "welfare" spending, dumping money into the "war on drugs", and a few other changes (like prohibiting anyone with a minor drug offense from accessing Pell Grants) occurred simultaneous to the decline. IOW, it's less that money is being spent than it is where that money is being spent. The Post WWII boom was enormous and fueled largely by the GI Bill and other government spending of the time that was directed toward people and infrastructure. There was also a lot of money spent on job training/college. Those investments paid off for decades.

I don't advocate forgiveness as an entry option. My first suggestion would be to apply the fiduciary standard to originating a student loan through a accredited institution much in the same standard as the investment industry is regulated.

These young people don't have money but they are indeed making an investment and they should be counseled with their interest as primary. They have parents who are not equipped to advise thrm of the value and return of the investment in a particular field of study. The corporate world would just as soon see the student loan market collapse as it gives them even more leverage to define the value of employment.

If you were retiring or leaving school for the working world, you needed to do it before the dotcom burst in 2000, 9/11, or the Great Recession 2007-2012, or the pandemic in 2020. If you were going through a major financial transition during any of these times with student debt or sustainable retirement hanging the balance your aspirations of starting a career, buying a home, starting a family, or retiring were likely impacted and supplanted by the need to sustain yourself by whatever means immediately available.

These events have spawned whole industries of worthless employment driving for Uber, making home deliveries. This jobs are necessity to the survival of millions of people. People who are lawyers, doctors, teachers, pharmacists doing this kind of work because they haven't found the stable opportunity in their field. You cannot build a life around this kind of employment. And the existence of this kind of employment is lowering the value of more traditional occupations. The time and the bills do not stop and the opportunity to course correct during it is vitally thin. The time to invest in new skills once out of school is a major commitment most people can't make.

If you haven't suffered the impact of any of this over the last 20 years, you probably have no idea how fortunate you are. In the same vein you probably are not the best guide for how to address this paradigm for those who only have their desire to do as well as their parents.

These young people don't have money but they are indeed making an investment and they should be counseled with their interest as primary. They have parents who are not equipped to advise thrm of the value and return of the investment in a particular field of study. The corporate world would just as soon see the student loan market collapse as it gives them even more leverage to define the value of employment.

If you were retiring or leaving school for the working world, you needed to do it before the dotcom burst in 2000, 9/11, or the Great Recession 2007-2012, or the pandemic in 2020. If you were going through a major financial transition during any of these times with student debt or sustainable retirement hanging the balance your aspirations of starting a career, buying a home, starting a family, or retiring were likely impacted and supplanted by the need to sustain yourself by whatever means immediately available.

These events have spawned whole industries of worthless employment driving for Uber, making home deliveries. This jobs are necessity to the survival of millions of people. People who are lawyers, doctors, teachers, pharmacists doing this kind of work because they haven't found the stable opportunity in their field. You cannot build a life around this kind of employment. And the existence of this kind of employment is lowering the value of more traditional occupations. The time and the bills do not stop and the opportunity to course correct during it is vitally thin. The time to invest in new skills once out of school is a major commitment most people can't make.

If you haven't suffered the impact of any of this over the last 20 years, you probably have no idea how fortunate you are. In the same vein you probably are not the best guide for how to address this paradigm for those who only have their desire to do as well as their parents.

Last edited:

Latest threads

-

-

-

SIAP there was an article that Joe K interviewed for assistant coach

- Started by mlingerfelt31

- Replies: 11

-

Final Home Midweek for Alabama Brings Samford to The Joe

Final Home Midweek for Alabama Brings Samford to The Joe- Started by Diamond Tide

- Replies: 0

-

-